Raising capital on your buy to let properties in order to grow your portfolio

The Guardian has recently highlighted an innovative way in which buy to let landlords can raise capital on their buy to let property via an interest-free loan, although doing so will cost them a share of their profit when the property is sold. However, if you are a buy to let landlord who wants to accelerate the growth of your property portfolio, the scheme is well-worth considering.

So what are the highlights?

- Top up your borrowing to 85% Loan to Value (LTV) by taking out a second charge loan of up to 20% LTV

- No monthly repayments – the landlord does not pay a penny in interest

- No additional debt service stress test

- For every 1% of the value of a property that it lends against, the provider of the Buy to Let Equity Loan will take 2% of the profit when the property is sold.

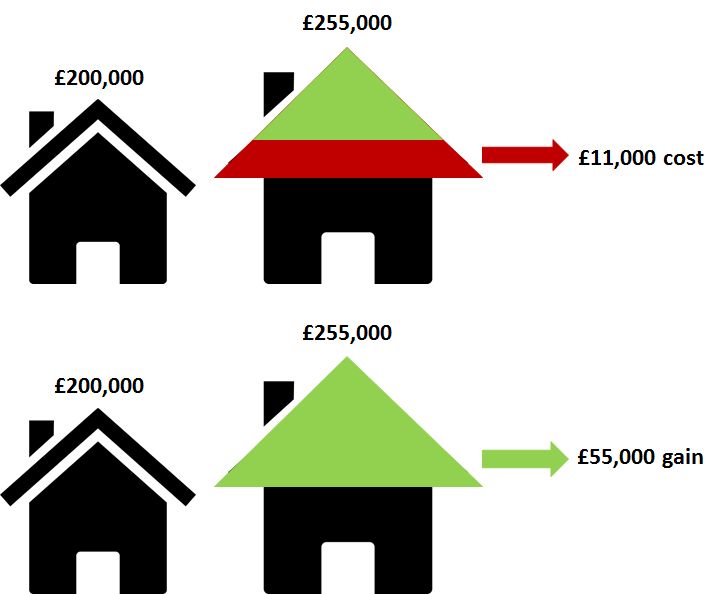

How about an example?

A landlord owns a buy to let property valued at £200,000 and takes out a Buy to Let Equity Loan worth 10% (£20,000) to raise some capital, to invest in another property worth £200,000.

Five years later, he sells the first property and, assuming average house price inflation of 5% per annum over the period, it fetches £255,000. The landlord has to repay the amount borrowed – £20,000 – plus a 20% share in the profit, which would be £11,000 (20% of £55,000). So in total he repays £33,000 – but during those five years has not paid any interest on the loan of £20,000.

Meanwhile, the property that he bought for £200,000 is also now worth £255,000 (assuming the same rate of house price inflation). On this property, the landlord has made a gain of £55,000.

The net effect is that he has given up 20% of the gain on the first property to receive 100% of the gain on the second. (i.e. the cost of £11,000 has enabled the gain of £55,000).

Are there any fees?

- Arrangement fee: 1% of the loan amount (£200 in the example above)

- Valuation fee: £195 plus VAT

- Early Repayment Charge: Year 1 only – the greater of 5% of the loan amount or the profit share

What are the risks?

You must repay the loan by the end of the term. If you don’t do this and do not have sufficient savings or cannot arrange another mortgage, you will need to sell the property, which may be repossessed if the loan is not paid when due. In addition, if the value of your buy to let property rises significantly, then the Equity Loan may cost you more than a traditional mortgage.

Any other relevant details?

- Minimum term for the loan is 1 year, maximum 10 years

- Minimum loan size £10,000, maximum £400,000

Next steps

As always with complex financial transactions, it pays to take the advice of an independent mortgage advisor, who will be able to assess your position and recommend the best way of raising capital on your buy to let portfolio, if that is what you wish to do. It may be that the Buy to Let Equity Loan is the right solution for you, but it might not be. An expert will be able to provide the advice you need for you to make the right decision.

Your home may be repossessed if you do not keep up repayments on your mortgage.