Equity release house value used to ease debt

18th Nov 2020

Equity release specialist Hamish Gairns explains how house value can be used to ease debt.

Posted in Equity Release

Read More

Equity release remote valuations and consultations

23rd Jun 2020

Equity release specialist Hamish Gairns explains remote valuations and consultations. The Equity Release Council (ERC) have been quick to respond to Covid-19 social distancing requirements. The ERC have approved remote property valuations and consultations.

Posted in Equity Release

Read More Equity release how unlocking house value liberates retirees

27th Jan 2020

Equity release how unlocking house value liberates retirees. Equity release specialist Hamish Gairns shares expertise on how house value is being used to liberate retirees.

Posted in Equity Release

Read More One in four consider lifetime mortgages

18th Jun 2018

One in four consider lifetime mortgages

Posted in Equity Release

Read More

Why lifetime mortgages are growing in popularity

18th Feb 2017

Why lifetime mortgages are growing in popularity

Posted in Equity Release

Read More

Generation rent explained; homeowner options

25th Jul 2016

Generation rent explained

Posted in Equity Release, Mortgages

Read More

Why lifetime mortgages can make sense for over 55's

20th Apr 2016

Why lifetime mortgages can make sense for over 55’s

Posted in Equity Release

Read More What is Equity Release? Questions and Answers.

26th Oct 2015

What is equity release?

Posted in Equity Release

Read More In your 60s? Equity release might improve your retirement.

29th Jun 2015

Are you over 60 years of age or do you have elderly parents that could benefit from releasing capital from their home? Equity release might improve your - or their - retirement lifestyle. Are you…

Posted in Equity Release

Read More

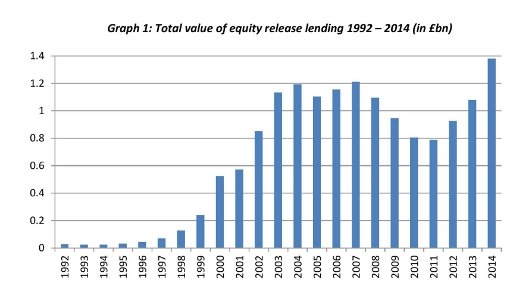

Largest amount of equity release lending ever recorded – £1.4bn in 2014

23rd Feb 2015

• Annual lending total is the highest since records began in 1992 • More than 21,000 new customers in 2014 – the most recorded since 2008 The total value of equity release lending reached almost £1.4bn (£1.38bn)…

Posted in Equity Release

Read More